DISCLAIMER: THIS IS NOT financial advice, this is not a trade or investment recommendation, nor is it A SOLICITATION TO SELL SECURITIES, WHICH IS ONLY DONE THROUGH APPROPRIATE DISCLOSURE DOCUMENTS AND ONLY TO QUALIFIED INVESTORS. WE ARE NOT FINANCIAL ADVISORS, NOR ATTORNEYS, NOR ACCOUNTANTS, NOR DO WE HOLD OURSELVES OUT TO BE SO. NOTHING ON THIS WEBSITE SHOULD BE INTERPRETED AS A RECOMMENDATION. as always, do your own diligence. this is opinion.

I’ve been an investor in one of PPR Capital Management‘s funds, otherwise known as PPR Note Co, for several months now, and am writing a review of my experience.

The abbreviation originally stood for Partners for Payment Relief, the name of their debt collection arm, noting PPR’s main function as a buy-and-rehab firm focusing on purchasing Non Performing Real Estate Loans at a discount, getting the debtors to start paying their mortgages again, and then reselling the now-higher-value notes for profit.

To do this at a greater scale, PPR raises money from investors, to whom it pays a Preferred Return in exchange for providing them capital to buy more notes. Essentially, PPR’s fund raises money from investors with a debt-like structure, uses that money to “flip” real estate loans, and pays the investors a rate of return, and pockets the difference.

In their now-16-year track record, they’ve never missed a payment to investors:

PPR Track Record Screenshots

While this is how PPR started, they have recently been allocating a minority of their portfolio to outright multifamily real estate investing deals, as well as lending money to flippers and developers. (Some people aren’t too happy about that, seeing it as a higher-risk investment than their primary investing thesis.)

What Returns Does PPR Pay?

PPR pays a fixed Preferred Return, depending on how long you lock up your money with them for. These returns have varied over the years in accordance with the cost of capital generally available in the market. As of November 2023, they pay 6-14% depending on whether you compound (reinvest) your returns with them, or not. Personally, I chose not to compound the $100k @ 12% investment I made with them, since I would rather have my income each month.

PPR Offered Returns

These offered returns are higher than those offered by Treasuries, say 10-Year Notes:

10Y T Bond Rates. Source: Macrotrends.net

But, with these greater returns come a greater risk level. PPR may have $322M under management and have been operating for 16 years, but that’s a lot less than the amount of time the US Government has been operating without defaulting.

So, my first suggestion is to think of PPR’s investment as being riskier than a Treasury. I think they would very much agree with that assertion, and I can’t think of anyone who would disagree. Some, like me, may simply be comfortable with taking more risk in a portion of their portfolio, and/or wish to diversify outside of Treasuries, for their fixed income goals.

The PPR Investment So Far

Having been an investor for the last 6+ months, it’s going well so far. Returns have been paid on-time via ACH distributions to my specified bank account, as promised.

PPR Returns So Far

The above snapshot was recorded from my Monarch Personal Financial Tracker transaction ledger. It’s possibly one of the simplest investments I’ve made: they really have taken steps to make it smooth to invest with them.

Customer Service & Investor Relations

One of the things that not every alternative investment fund manager does well is provide good investor relations, aka customer service. PPR is a standout exception here. Every email I’ve gotten from PPR’s investor relations reps has been friendly, timely, knowledgeable, polite, and all the things you’d want in a rep:

PPR Customer Service

It’s become a surprisingly big deal for me to want fund managers to provide what I would call good customer service. By the converse, when a fund manager’s team provides poor service, it says something negative to me about how they run their fund, and how they handle my money. There isn’t always a correlation there, but responsiveness is important to me, especially around funding.

PPR Complaints

I have not been able to find any reports of investors who invested with PPR and didn’t receive their money back. Everyone who I’ve found, such as on BiggerPockets and Reddit, has had a similar experience as I have. Nor could I find any investor complaints about Dave Van Horn, Steve Meyer, or any of the other leadership team members.

Overall, this has been a positive experience. I’m getting regular income distributions, and PPR’s team has been great to work with. This investment has risks, and PPR could stop paying distributions any time. The worse case is that I might lose all of my money. That said, I’m comfortable with PPR’s investment strategy, their team, their track record, and ultimately with their place in my portfolio.

Feel free to leave a comment if you have any questions.

ATM INVESTMENTS Disclaimer: This is not a solicitation to sell securities, which is only done through appropriate disclosure documents and only to qualified investors. We are not financial advisors, nor attorneys, nor accountants, nor do we hold ourselves out to be so. Nothing on this website should be interpreted as a recommendation. investors are encouraged to consult with their personal legal and tax advisors. Neither this website nor its representatives, officers, employees, affiliates, sub-contractors or vendors provide tax, legal or investment advice. Nothing on this website is intended to be or should be construed as such.

We sat down for coffee and soon began to talk about investing.

“Well, the most recent investment I made was another tranche of $52k into an ATM fund”, I told my friend.

His response was typical. One raised eyebrow, a quick blink as he did a double take, and then a couple seconds later, his reply: “What? Why… what do you mean?”

No surprise. It isn’t obvious how ATMs – yes, automated teller machines, those! – could even be called an investment. What would you be investing in, and does this mean the investor is shuttling cash around the city in armored cars, withdrawing from here and depositing there?

As we’ll get to: buying, placing, funding, and operating your own ATM is a valid strategy. This article isn’t primarily about how to start an ATM business, but we’ll direct you toward resources that can help, if you want to go this route.

Instead, this article is mostly about how I passively invest in ATM funds, and earn a 14-16% Internal Rate of Return on my capital (and an even higher Cash On Cash return), in a very tax-deferred way. Completely legally.

Snapshot of my monthly payments from my online checking account

Of course, the main friction point is the set of risks this comes with. First, you need to be an Accredited Investor to invest passively in ATM funds. If you’re not accredited, then you should first try to become so. But why do you need to be accredited? Because the risks of ATM investing are much less obvious than the risks of buying ETFs and public stocks, and the government doesn’t want people who can’t afford to lose money, to be sucked into real estate syndications – which ATM funds absolutely count as! – without first having a sophisticated understanding of exactly what they’re getting into.

For me, this means I don’t want to allocate more than 5-10% of my portfolio to ATM funds. For you, this might mean something different.

Let’s get into it.

Rather watch a Youtube video about this? Click below.

What does it mean to invest in ATMs?

Like any investment, you must understand what it is exactly that you’re getting into.

The primary revenue stream of an automated teller machine, or “ATM”, is the transaction fee. You know… the $2-3 you have to pay to withdraw cash from an ATM. Stack 10-20 transactions a day, and you have a perfectly viable and understandable small business.

A single well-placed ATM in a high-traffic area should yield between $800 to $1,300 per month in revenue.

What’s a high-traffic area? It should be obvious if you start paying attention to this in your daily life: Pharmacies, cannabis dispensaries, music festivals, casinos, bars, grocery stores, etc all often have ATMs on-site, where you can withdraw cash if you need to. Banks have them too of course, and as we’ll see later, some ATM investment fund operating companies also serve banks.

Don’t take that as gospel, of course. If you buy your own ATM (we’ll get to that in a minute), you might easily lose money on it, if you aren’t good at placing machines or establishing agreements with property owners who will rent you space to put them in.

Think of it this way: operating an ATM is essentially a retail micro-business, with an average transaction size of a few bucks, and no full-time employees to manage. If you can do it with one machine, you can do it with 10, 100, or thousands. There are about 450,000 ATMs in the United States at the moment, and a few million around the world.

Like any business, it can have investors.

The question for you is: do you want to be the one hustling around the city with cash, and earning much more of your fee revenue? Or do you want to invest passively in a fund that does this for you and takes a cut?

Active Investing as Owner/Operator: Should You Buy ATM Machines?

You can find videos aplenty on Tiktok purportedly showing you how to start an ATM business as a side-hustle. And what a hustle it is… every few to several days, you’re getting more cash from the bank to deposit to your ATM, so it doesn’t run out of money. It’s not that this is an invalid way to make money, but at this point, you’ve bought yourself a job. And a very effortful one, at that.

How much do ATM owners make? About $450-700 per ATM per month, if they’re independent and can place their machines in at least moderately good locations. And you’re in control of your “jobvestment”, which is a nice bonus. Unless you physically get robbed (possible, of course), you know that nobody’s stealing from you.

But there are a few problems with this jobvestment that you’ve bought yourself:

If you want to hire, you better REALLY trust your employees. They’re shuffling your cash around the city for you. Better dial in your audit procedures.

If you don’t hire this out, good luck taking a vacation. Ever.

You need a lot of ATMs to make this profitable.

You’re going to need to be really good at sales to build up the relationships you’ll need with property owners, to convince them to lease their space to little ol’ You, and not your Much Bigger ATM Operator Competitor. You might need to outbid the bigger competitor, or just settle for lower-quality spaces. As a fun exercise: pretend you already own an ATM, and cold-call the 20 most likely possible locations in town. I bet you 19/20 of them already have an ATM, or won’t deal with you even if they might have space available.

Your bookkeeping is going to suck. Cash based businesses are prone to IRS audits, too. Not to mention Independent ATM Deployer (IAD) audits, if you’re certified.

And then some.

As an experienced entrepreneur myself, I can tell you this: there are much easier businesses to run in this digital age, that don’t require rucking bags of cash around the city.

So, despite the risks of passive ATM investing (primarily: giving up control), I do invest in ATMs through funds. I just don’t put more than 10% – maybe temporarily 15% – of my portfolio in them at any given time.

By the way: It’s “ATM”, not “ATM Machine” (the latter is redundant)

Passive Investing In ATM Funds: Risks To Know Before You Invest

In the passive investing model, you’re not buying your own ATMs, you’re not stocking them with cash… you typically don’t even know exactly where the ATMs that the fund operates, are. You’re an investor in a fund whose business is to owns and operates ATMs, take a cut, and pay out some of that to you. Suddenly, the picture changes: you’re staking your investment on the belief that the fund operator is better than you would be at the whole game of buying, placing, updating, managing, funding, and supporting ATMs. You’re hoping that, with their institutional knowledge and their master service agreements with Walgreens chains and grocery store conglomerates, they’ll have operational efficiencies that you couldn’t have as an independent operator with your own “paper route” and your 5-20 machines you bought on a marketplace site.

But you’re also hoping that the fund doesn’t become a Ponzi scheme, and that its operators remain honest. In fact, it’s a pretty safe bet that anyone experienced in the ATM business would be “better at it” than I would, with no ATM management experience. The biggest risk in passive ATM investing is actually the fund managers’ integrity. This is a far bigger risk than the macro risk of a widespread and immediate reduction in the use of cash (and therefore ATMs) in the United States – which is still a risk, but in my view a smaller and more manageable one than the Ponzi scheme risk.

Ready to take that risk – which is a factor in all investments but an even greater priority in private ATM investing? For me and for other investors I know, the potential rewards of this asset class make the risk worth taking. Read on for more details about the returns and tax benefits being offered by ATM funds.

Speaking of knowing the operators you’re dealing with: one of the interesting tidbits you’ll learn about this space is that almost every website you will come across offering ATM fund investing, is actually a feeder for a company called “The Real Asset Investor”.

Who is The Real Asset Investor?

Founded by Dave Zook in 2015, The Real Asset Investor is a niche investment fund. Their strategy is to find asset classes that produce cash flow and/or equity growth, with preferential tax treatment. And ATMs have been one of their most popular investment offerings since then. Essentially, TRAS brings in capital, and deploys it with the ATM operator, Paramount Management Group, which is a pretty run-of-the-mill-looking managed services business, per their LinkedIn, focused on automated teller machines. There are shareholders from TRAS on the board of PMG, and vice versa.

If you’re passively investing in ATMs, there’s a good chance that Dave Zook’s company or its affiliates are raising money to be deployed in Paramount’s ATM management model. I say all this merely to let you know who the players are and what’s happening with your money when you invest it.

Like I touched on above: the biggest risk isn’t that Paramount is bad at operating ATMs, the risk is that TRAS or PMG end up becoming fraudulent. As best we can tell, based on the fact that Paramount acquired another ATM company back in February 2023, and because Paramount’s activities are audited by a bank, they seem to be a normal, healthy operating business.

As always, with any private syndication but especially with one that is somewhat opaque and cash-based where there isn’t one single property you can just go visit in person (like a multifamily syndication), keep your eyes peeled and don’t assume that an honest fund operator won’t later become dishonest, down the road. It’s happened before, and it will happen again. And do your own diligence on any ATM investments you make.

Now, let’s get to the good part: what are the potential advantages of investing in an ATM fund?

Advantages of Investing in ATM Funds

Investing in ATMs, even indirectly via a fund, can offer investors several advantages, especially if they are interested in generating a predictable cash flow. Here are some of the reasons why:

The asset value doesn’t matter. Who cares if the ATMs go down in value? In fact, we expect them to. We expect the ATMs to be pretty much obsolete and valueless, within several years. We’re not investing in ATMs for their asset prices, we’re investing in the cash flow stream that comes from the transaction fees. Relatedly…

Accelerated tax depreciation. ATMs depreciate in value very quickly, and as of the time of this writing, at least for my own situation, 60-80% of the value of my investment can be expensed as depreciation in the first year. The rest is depreciated in the the handful of years following the first. Got any passive real estate income? This depreciation expense can be a significant write-off against that income, kicking the tax can down the road. Consult your tax professional with any questions on this: I’m not a CPA, I’m just my CPA’s client.

Predictable Income. ATM investments, at least through The Real Asset Investor, pay me a fixed monthly return starting in 2-4 months after the investment is made. They deposit these payments via ACH directly to my bank. This is very similar to the structure that PPR offers, and that you can get with buying high-quality real estate notes.

No Asset Management Labor. There’s literally no work involved apart from making sure that the payments arrive on time.

Higher-Than-Average Yield. Without even factoring in tax depreciation, ATM fund investments offer advertised cash-on-cash returns of over 24% per year, despite there being little to no return of principal at the end of the 84-month term. Even factoring in the lack of returned principal, the advertised IRR can come in north of 14% per year. That’s lower than many real estate syndication operators offer, but the cash flow compounding aspect is the real magic factor in play. Principal is expected to be paid back within a few years, and the rest is gravy.

Low Correlation with Markets: ATMs are not correlated with stock and bond markets, which makes them a good diversifier in a portfolio. In periods of stock market volatility, these notes can provide a more stable source of income. The main risk here is that people stop using cash in extremely significant quantities; but, while you and I probably rarely use cash, significant segments of the population still use cash quite a bit.

Passive “Mailbox Money” Income: The best advantage of all! Once the ATM investment is made, there’s no work required of you as an investor.

These advantages, for me, outweigh the very crucial risks, as we delved into above.

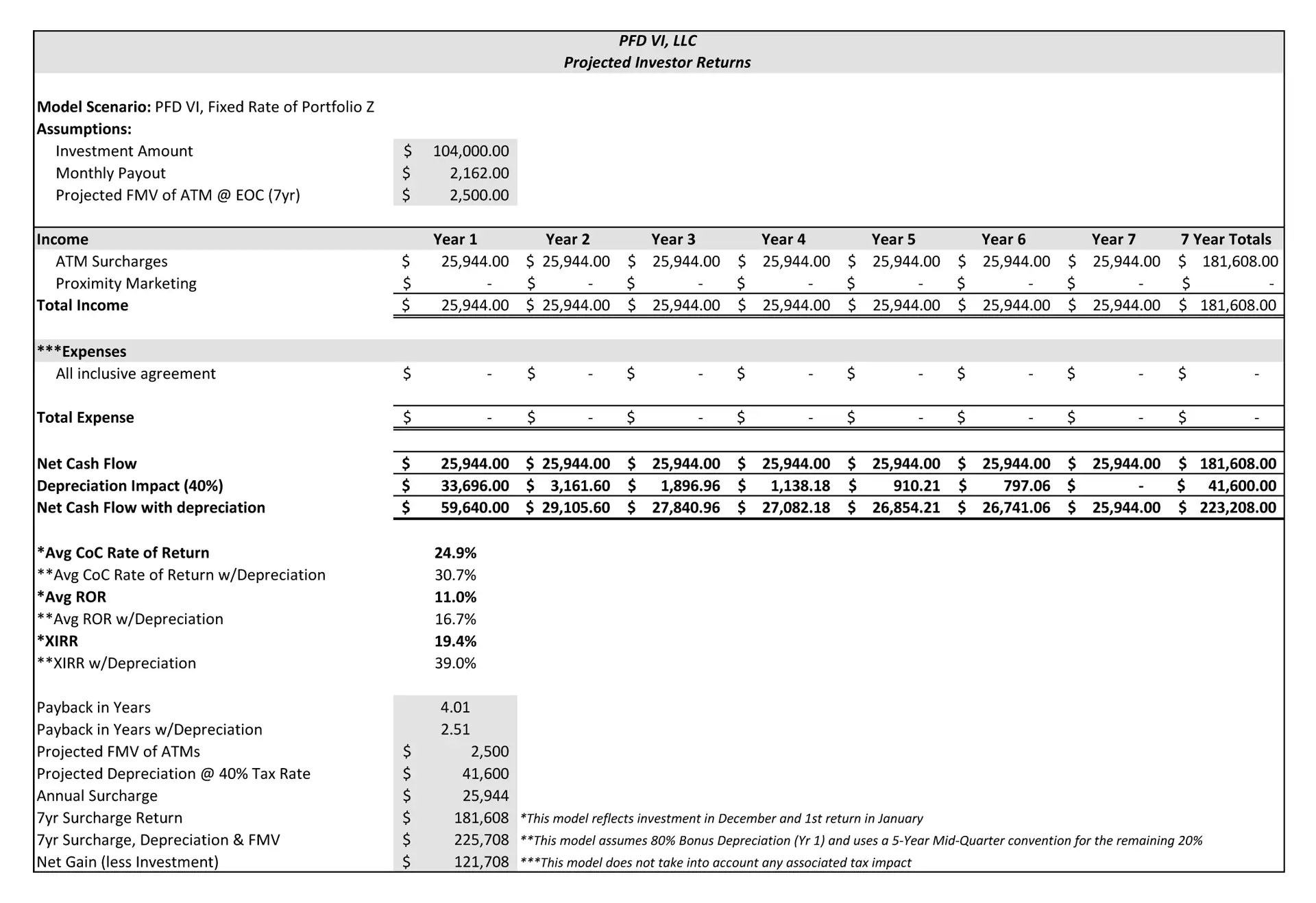

ATM Investments: Advertised Returns

As the fund’s website clearly states:

IMPORTANT: The projections or other information generated by the cash flow model above regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results.

Pay close heed to that disclaimer. Nothing in business or investment is guaranteed. With that being said… the following table of returns is advertised by the most popular ATM investment fund available today.

Source: https://therealassetinvestor.com/portfolio/atm-investment-summary; Depreciation Impact is calculated assuming a 40% tax rate; you should substitute your own tax rate here, and contact a qualified professional for specific advice you may need about the tax impact of this investment.

A full model to help you calculate the projected, advertised returns of the ATM fund I've invested in. Past performance does not guarantee future results.

My view as an investor in this fund is that ATM investments are worthy of a small percentage of my overall portfolio, for a few reasons: the amount I’ve invested cumulatively is one I can afford to lose; the bonus depreciation will defer my taxes payable on this and other passively-earned income; the cash flow begins quickly and lets me compound my gains by reinvesting it earlier, elsewhere; and of course, the overall rate of return is quite good. It solidly fits my goal of earning passive, tax-advantaged income without adding more work to my plate.

Good luck, do your own diligence, and remember: I’m an investor, not a financial advisor. Go make your own mistakes, and also, if you can: make a bunch of your own money.

When I talk to people about investing in mortgage notes, I usually get a confused look: “Wait, what do you mean? I have a mortgage on my house, is that what you’re talking about?” My answer is: “Kind of like that, yes. But when I buy a mortgage note, I’m the bank, not the borrower!” Then, they become curious!

But even though mortgage notes can return 9%, 14%, or even up to 20% rates of return or more – with a fixed rate of monthly ACH income! – why don’t more people know about these investments, or participate in them? After all, with no volatility and higher rates than stocks or bonds, they seem like a sure bet.

Not so fast.

While these investments are perfect for some, they’re definitely what I would call ‘alternative’ investments, in that you can’t buy them from your Robinhood account, and you can’t trade them like a stock on your mobile app. If you want to get into mortgage note investing, you’re going to need a little creativity, and to put in a little work to actually find good notes to buy.

This article will go over:

what mortgage notes are

how to invest in them

the risks of buying private notes

why investors should consider either investing in notes through funds, or by buying what are called ‘partials’.

That way, you’re not dealing with foreclosures and needing to potentially make debt collection calls to borrowers, yourself. (Because then it’s not an investment, it’s a business!)

Let’s get into it.

What are Real Estate Mortgage Notes?

A real estatemortgage note is like an IOU backed by a property. It’s the property owner saying “I promise to pay you back this loan, and if I don’t, you can take my property.” Simple as that.

Now, there are two sides to this – the promissory note and the security instrument (which can be a mortgage or a Deed of Trust, depending on where the property is located). The promissory note is the borrower saying “I’ll pay you back,” and the security instrument is what makes their promise carry weight. It ties the note to the property via a lien. So, if the borrower doesn’t pay as agreed, the lender (mortgage note owner) can sell off the property. (The catch here is that with a Deed of Trust, the lender can sell the property without going to court. With a mortgage, they have to go through the legal hoops to do it.)

For example, let’s say you’re buying a house that’s $270,000. You only have $55,000 cash, so you borrow $215,000 from a lender. To get that money, you sign a promissory note saying you’ll pay it back, and a mortgage tying your promise to your new house. If you can’t pay, the lender can take your house as payment. That’s the gist of it!

Again, that’s how a mortgage note works when you’re the borrower – but remember, you’re not borrowing, you’re on the opposite side of this transaction as the lender.

What Are The Different Types of Notes?

The main kinds of real estate notes you can invest in are called Performing Notes and Non-Performing Notes. In the industry lingo, you’ll also hear about “senior liens” (“first liens”), and “junior liens” (“second liens”), too. All that means is that the senior position has less risk, and gets paid first if there’s a loss, so be careful when buying second-position notes.

1. Performing Notes (PNs) are where the borrower is making their scheduled payments. The main thing that matters in this case is how much income the note offers now, since if you buy this note, that’s what you’ll be getting.

2. Non-Performing Notes (NPNs)are where the borrower is at least 90 days behind in making their scheduled payments. In this case, if you buy this note, you’ll have to negotiate with the borrower to restructure the terms of the loan (more grace period, good-faith payments, reduced interest rate, reduced balance, and other options are at your disposal). Or, you’ll need to foreclose on the property. The potential returns here are seriously good, but the risk is commensurately higher, and at this point, it’s less of an investment you’re making, and more of a business you’re running. (You’ve never had to get on the phone with the managers of AT&T and negotiate your dividend, have you?).

What Are The Ethics of Buying The Rights to Someone’s Mortgage?

When it comes to NPNs, some funds and asset managers specialize in residential non-performing real estate loans: they have a system for calling property owners, informing them that they’re serious about collecting on the mortgage, but they also remind the borrowers that they’re understanding. The new mortgage owner is willing to restructure the terms of the loan, to get the buyer back on track, in a way that’s favorable o the borrower. Needless to say, many homeowners really appreciate this. NPN funds have helped countless numbers of homeowners stay in their homes, at the expense of big banks who didn’t want to deal with the renegotiation or who aren’t able to due to regulations.

And that’s just wonderful.

Advantages of Investing in Mortgage Notes

Investing in private mortgage notes can offer investors several advantages, especially if they are interested in generating a predictable cash flow. Here are some of the reasons why:

Be The Bank. Have you ever thought you might like to invest like a bank does? (Well, apart from First Republic and Silicon Valley Bank, that is.) This is your chance to take the other side of the home borrowing equation. Instead of signing up for years or decades of monthly payments, you’re signing up for monthly cash flow.

Predictable Income: Private mortgage notes pay interest at a set rate, and you receive payments monthly according to the amortization schedule. This makes them ideal for investors who want a predictable income stream.

No Property Management: Woo hoo! No fixing toilets, no tenant relationships, no nothing. Well… except in the unlikely but possible event that you have to foreclose. It’s out of your hands. The borrower is the property owner, therefore typically very incentivized to maintain their property and keep it in good shape.

Higher Returns: Since notes carry higher risk and are less well-known than traditional investments like treasury bonds or CDs, they almost always offer higher interest rates – generally even higher than bonds and fixed-income ETFs.

Security: Mortgage notes are secured by the underlying real estate property (be very careful if you’re offered a promissory note investment that actually has no security except the borrower’s promise to pay!). In case of default on a secured note, the investor can foreclose on the property to recover their investment. This collateral makes these notes relatively secure, unless the property can’t be sold for enough to recover their investment – which can happen if you buy the wrong note.

Diversification: Buying private mortgage notes can offer a way to diversify an investment portfolio, and improve cash flow. They offer a different risk-reward balance than stocks, bonds, or traditional real estate investments, which might reduce overall portfolio risk.

Control: As a private note holder, the investor can pre-select the terms of the loan, whereas corporate or government bond ETFs are entirely out of your control. With private notes, investors can negotiate interest rates, repayment periods, and other terms, which can help you stay comfortable and in-the-know about how your portfolio is doing.

Ability to Buy at a Discount: One aspect of you having control over this investment is that you can simply “lowball” or offer less than the Unpaid Balance (UPB). Depending on whether a note is performing or non-performing, it might trade at a 10-80% (!!) discount from its UPB. Of course, a huge discount likely indicates the note is in terrible shape, and will need significant rehabilitation to get it back to a performing state. If you acquire the note at a discount, or participate in a fund that does this, it’s the equivalent of you earning a much higher yield than the borrower is paying in mortgage interest. For example, if you’re earning a healthy 10% on a note, the borrower isn’t necessarily paying that much in interest – you might just have bought the note from a bank at a discount, and thus increased your yield.

Low Correlation with Markets: Mortgage notes tend to have a lower correlation with stock and bond markets, which makes them a good diversifier in a portfolio. In periods of stock market volatility, these notes can provide a more stable source of income. Obviously if the economy is doing terribly, it’s more likely you’ll need to foreclose on the property in the case of default, but that likelihood has historically never gotten quite too high.

More Liquidity Than Many Alternative Investments: Even though it’s harder to sell a mortgage note than a public stock or ETF, it’s very possible. There are plenty of note buyers available for the average investor to sell to (although you might be taking a haircut if you do so).

Passive “Mailbox Money” Income: The best advantage of all! Once the mortgage note is purchased, it generally requires little management unless the borrower stops paying, making it a more passive investment compared to direct real estate investments, which require active involvement in management and maintenance.

As we began to touch on, investing in private mortgage notes also comes with risks. They can be more complex and are absolutely less liquid than popular capital markets investments. There’s also the risk of default, which means the investor might have to deal with foreclosure proceedings – which is not impossible to deal with, but still a burden. It’s important to do thorough due diligence before investing in private mortgage notes, including understanding the borrower’s creditworthiness and the value and condition of the underlying property.

How To Buy To Real Estate Mortgage Notes

Buying Notes Directly

Unless you know of any private mortgage note holders that have good quality notes lying around to sell to you, you’ll need to get out there and pound the pavement, in a sense, if you want to buy mortgage notes directly. Here are some ways to do that:

You can also find a mortgage note broker through forums or trade shows, although make sure to do your due diligence, because the broker isn’t going to do it for you

For-Sale-By-Owner property owners in your local area, as well as real estate investment groups, might also be good lead sources for you.

An thorough overview of mortgage note investing, if you want to make it your primary business. The author, Eric, is also an excellent person to network with, and - if you wish - offer to buy partial notes from.

We earn a commission if you make a purchase, at no additional cost to you.

04/26/2024 03:03 pm GMT

Investing Via a Fund or Platform

A much-easier way to invest in mortgage notes is to do so through a fund that professionally acquires and manages the notes. This is how to make note investing a truly-passive endeavor, since if you’re buying notes directly, you’ve become a debt collector and administrator of a lot of paperwork.

Don’t take these as personal recommendations, and do your own diligence. That being said, here are some of the places I’ve invested, directly or indirectly, in mortgage notes through a passive investment vehicle:

I receive monthly income from all of those, from my mortgage note investments. However, I generally shy away from tech-enabled investment platforms, and as such limit my exposure to Fundrise and Yieldstreet etc to no more than 2-3% of my portfolio.

Buying Partial Notes From Note Holders

Yes, you can split a note into multiple parts! If this sounds complicated – it’s not, really. Whichever mortgage servicer is managing the loan can break up the monthly payments they receive from the borrower, to multiple parties.

But why would you as an investor want to buy part of a mortgage note?

Well, your contract as an investor is not with the borrower, but (ideally) with a professional, well-capitalized mortgage note investor whose business it is to manage notes. They take on any debt collection that has to be done, as well as any foreclosure responsibilities. If you buy a partial note, you won’t need to call the borrower for any reason. In fact, the initial note holder will ask you not to do this. That removes one of the biggest hurdles in mortgage note investing, which is when you end up becoming a “mortgage note management business owner”, rather than a passive investor.

Okay, but now: why would the mortgage note holder sell you part of their note, if the note is so great?

Primarily, because they’ll offer you a lower rate of return than they’re getting, and they get to recapitalize. For example:

Jack directly owns a Note with a balance of $25k, paying them a 16% yield.

Jill has a target rate of return of 12%, and wants to invest $25k.

Wonderful! Jill buys the Note from Jack for $25k.

Jack now receives a monthly 4% yield on a $25k note, while having no capital in the deal. That’s kind of cool. They get to go buy other notes – say, ones that have even better returns. Or they can invest in whatever they’d like.

Jill reaches their target rate of return of 12%.

If anything goes wrong with the note and the borrower stops paying, Jack has to step back in and make Jill whole, so Jack had better be good for it and be ready to do that if necessary.

Jill gets the lower return in this scenario, but is more like an ‘investor’. Jack gets a higher return, but puts more of their time at risk. Jack is more like a business owner.

Risks for Investors When Buying Mortgage Notes

There are a lot of risks to think about when you’re looking at these ideal-seeming investments. Yes, they often have great rates of return, and passive income. While those are advantages, keep these risks in mind:

The borrower stops making payments. This is the big and obvious one. If you own the note directly, it’s on you to get the borrower to start making payments again, and you need to stay within legal debt collection guidelines as you do so. If you own a partial note, the person who sold you the partial will need to make you whole however it’s listed in your contract.

You bought a fraudulent note. If you didn’t do your diligence on the property or the borrower, you might have bought a worthless piece of paper with no security in it. That’s why due diligence is so important. It’s much less likely that AT&T is a scam, than the guy you found online offering to sell you a note he owns.

You need to foreclose, and the underlying property isn’t worth enough to make you whole. Ouch. You need to foreclose, but when all is said and done, even after a hugely burdensome process with a borrower who didn’t engage with you and abandoned the property in bad shape… you can’t sell the property for enough to repay yourself. To add insult to injury, the foreclosure process made you incur legal and other fees.

Interest rates increased and you tried to sell your note. This makes your note worth less, because people are less willing to buy fixed-rate debt when variable interest rates in the marketplace rise. Who would buy your 7% private note, if a 10-year Treasury pays 5.8%?

The real estate market is way down. If the market is down and your borrower doesn’t see any path to getting back on track from being underwater, they’re much more likely to walk away from the property and leave you with it. Probably in bad condition.

You tried to collect on your debt improperly in the wrong state, and broke the law. Remember, the borrower’s locationand property location matter. If you own notes directly and you say the wrong thing when you call the borrower, you could be breaking the law.

You need cash now, and you’re having a hard time selling your note for a good price. No Robinhood is coming to save you. The beauty and curse of mortgage notes is that they’re not very popular. You’re going to find many fewer buyers for them, if you need to unload the investment.

You bought a partial note from a not-creditworthy owner. The borrower stops making payments, the note goes into default, and now you’re trying to be made whole on your partial note investment from a note holder that can’t make good.

You forgot that this is still a real estate investment. If you have your entire portfolio in real estate, buying mortgage notes is only somewhat a form of diversification. It’s still a loan… backed by real estate. Real estate goes up and down.

You were expecting FDIC insurance. Nope. This isn’t a bank account. There’s no SIPC, FDIC, or any other acronym coming in to save you if things go bad. You’re on your own with your wits and, hopefully, a good attorney.

This part of the industry is lightly-regulated. This isn’t like buying a home you live in and getting a mortgage for it from a bank, where the federal government is controlling a lot of how banks and brokers can lend to you. Now you’re on the other side. If someone sells you a bad note and runs off, you’re going to have a hard time getting anything back.

That’s quite the list. Remember, there’s no free lunch in this world: if you learn intensively about an asset class, especially about how to manage your risk, you’ll give yourself a much better shot.

And that’s exactly what I recommend you do: read, consume information, experiment with small amounts of capital, and: network, network, network!

Conclusion

Buying real estate mortgage notes as investments can be a great addition to your portfolio, or it can even be a business that you actively manage. Don’t forget about the key risks involved, do plenty of diligence, and – most importantly – enjoy this asset class for what it can be, at its best: a wonderfully-passive vehicle and a relative secret among the average crowd of investors.

Good luck.

Disclaimer: This is not a solicitation to sell securities, which is only done through appropriate disclosure documents and only to qualified investors. We are not financial advisors, nor attorneys, nor accountants, nor do we hold ourselves out to be so. Nothing on this website should be interpreted as a recommendation.

Just a quick note today about a new addition to the articles on Mindfully Investing. If you’ve been a regular reader of Mindfully Investing, you might have noticed that I’ve done a series of posts in the last few months on so-called “alternative” investments. These are investable items beyond stocks, bonds, and cash, which are the main focus of Mindfully Investing. Alternative investments that I’ve covered include:

Real estate

Gold

Annuities

Commodities

Currencies (foreign exchange and cryptocurrencies)

Peer-to-peer lending

Derivatives (options and futures)

Collectibles and art.

I compiled these posts into the newest of the foundational articles that describe the Mindfully Investing philosophy. You can find Article 9. “Alternative Investments” here.

If you’ve read all of my posts over the last few months, first I thank you. But more to the point, you probably won’t find anything too surprising in Article 9. On the other hand, if you’ve missed some of my recent posts, or found them too long (or boring) to wade through, then the Article 9 provides a shorter summary of all that work. I figured that some folks might find that helpful. Happy reading!

My last post was the first in a two-part series about the cornucopia of alternative investments. Mainstream investments like stocks and bonds can sometimes seem like stale white bread as compared to the wagon loads of fresh-baked alternative investments available to individual investors. In today’s post, I’ll finish perusing the buffet of alternative investments by evaluating:

Peer-to-peer lending

Derivatives (swaps, forwards, futures, and options)

Collectibles and art.

Like my last post, I’m going to resist a made-from-scratch evaluation of these three alternative investments. Instead, I’ll use the four cornerstones of mindfulness (rationality, empiricism, humility, and patience) as a quick recipe to evaluate whether any of these are worth considering further.

Peer-to-Peer Lending

Peer-to-peer lending is a way for borrowers to get loans directly from individual lenders instead of from conventional lending sources like banks. The individual lender is investing their money by loaning it to one or more borrowers who are contractually obligated to return the loan, plus interest, within a specified period. So, peer-to-peer investing returns come entirely from the interest paid back on the loans.

Peer-to-peer lending dates back to at least the time of the Bible, which has several verses about loans between people, as well as from “banks”*. Because it’s often difficult for individual investors to find reliable borrowers, banks and similar financial businesses have historically served as the link between people with money and those who need to borrow, while profiting handsomely from the exchange.

But the internet is slowly disrupting this long-standing intermediary function of the banks. Peer-to-peer lending platforms sprung up in the early 2000s and have grown into a business that transacts $86 billion dollars in loans. Unlike banks, peer-to-peer lending websites don’t make money from charging interest to borrowers; instead they charge fees on the facilitated transactions. There are many peer-to-peer lending platforms that focus on different types of loans including:

Returns – I quickly found recent and credible accounts of investors obtaining anywhere from 2% to 11% annual returns from a few of the larger peer-to-peer lending platforms. The platforms themselves report investor annual returns anywhere from “less than 0%” (losing money) to “greater than 15%”. One popular platform reports the most common annual return for less risky portfolios as 6% to 9% and for more risky portfolios as 9% to 12%.

Given that the average annualized returns for stocks since 1871 is about 9.0%, a potential annual return in the 9% to 12% range sounds appealing. But of course the devil is in the details. To get those higher returns, you need to loan money to people who have a higher risk of defaulting (not paying you back). And finding the right balance between a good return and reasonable default rates depends on the focus of each platform, how it’s operated, and many other details.

Risks – The major risk with peer-to-peer lending is defaults. The main way peer-to-peer platforms reduce this risk is through diversification. For example, instead of loaning your entire $10,000 investment to one person, most platforms suggest or require that you spread that money around to many borrowers. For the borrowers, that means their loan is coming from a group of investors, and the interest paid back is split among that same group of investors. The platform does all the work of making sure the correct amounts of money get into the right hands on both sides of the transaction. So, if one borrower defaults, many investors take a small ding in their return, which greatly diminishes the risk of negative returns for any individual investor. Some platforms also maintain reserves or insurance that they can use to minimize the impact of defaults on collective returns.

Of course, the return you get is highly dependent on the default rate within the group you’re lending to. While all the platforms factor past defaults into future return estimates, the default rates are necessarily based on past data. Given that most of these sites have existed for 10 years or less, the track record for these default rates is an order-of-magnitude less than the 147 and 94-year histories of U.S. stock and bond returns, respectively. Past default rate estimates may be even less predictive of future rates because of changes in the economy or platform operating rules over the years.

I reviewed some personal anecdotes from various bloggers to get some sense of the potential divergence between expected return estimates and actual returns, which is one way to summarize default and other risks involved with peer-to-peer investing. This table compiles the results.

You’ll note that actual returns above 9% were pretty rare. Excepting the oldest result, the actual returns were 1% to 5% lower than the investor originally expected. Yikes!

Given that peer-to-peer lending is a relatively new industry, the potential for platforms to go out of business is another risk. U.S. regulations require that platforms have a plan for resolving loans after a company “failure”. But it seems unlikely that such plans insure zero impact on investor returns, considering all the unexpected issues and chaos normally associated with a large business dissolving.

In terms of both returns and risks, peer-to-peer investing is remarkably similar to high-yield corporate bond funds (often called “junk” bonds). Like high-yield bond funds, peer-to-peer investing provides access to riskier high interest rates, while mitigating some of that risk through simultaneous exposure to many borrowers. It’s not surprising that peer-to-peer returns are becoming more aligned with the prevailing interest rates for high-yield bond funds; both are around 5% to 6% per year or less.

Therefore, the mindful conclusion about peer-to-peer investing is like earlier Mindfully Investing conclusions about high-yield bonds. Specifically, mindful investors should focus mostly on stocks. To the extent your portfolio has some bonds to cushion against short-term stock declines, using high-yield bonds simply pushes your overall portfolio into a more risky profile that’s similar to holding more stocks instead. Holding too much risky high-yield bonds, or peer-to-peer loans, starts to defeat the purpose of holding a combination of safer bonds and more risky stocks.

Derivatives

A derivative is a contract between parties where the value of the derivative is based upon an underlying asset or financial instrument such as stocks, bonds, commodities, currencies, or groups of such assets like an index. The most common derivatives include a contractual agreement where parties:

Swap – Exchange one cash flow from some underlying asset for another cash flow under specified conditions in a “non-standard” contract (a contract devised by the parties involved).

Forward – Buy or sell an asset under a non-standard contract at a specified future time at a price agreed upon today.

Future – Buy or sell an asset under a “standard” contract (a contract devised by an intermediary) at a price agreed upon today (the futures price) with delivery and payment occurring at a specified future date.

Option – Give the buyer the right under a standard contract, but not the obligation, to buy or sell an underlying asset at a specified price on or before a specified date.

These derivative types are often further sub-categorized by the underlying asset involved, how they pay off, and the manner in which they’re exchanged. There are even more complex derivatives such as credit default swaps, which were a key factor in the 2008 financial crisis, and collateralized debt obligations, both of which are only distantly related to an underlying asset. There are many more flavors of derivatives that I won’t attempt to describe here. But if you’re interested in finding out more, Investopedia is a good place to start.

Derivatives are mostly used to manage investing risks. Depending on which side of the derivative contract you’re on, you can use them to either decrease risks associated with the underlying asset (called a hedge) or take on more risk in the hopes of achieving a higher returns than would be available from investing directly in the underlying asset.

Returns – Because of the very nature of derivatives as a risk management tool, it’s impossible to generally characterize the returns available from derivatives. Returns can vary from massive losses to theoretically astronomical positive returns. The returns are entirely dependent on the particulars of the obligations and rights under the derivative contract.

Risks – For the same reason, it’s impossible to generally characterize the risks from derivatives. It’s easy to buy a future or an option that loses money. But that’s not always a bad idea. For example, you might end up losing a bit of money in return for insurance against losing a larger amount of money from exposure to an underlying asset. It’s just like paying insurance premiums, even though your house didn’t burn down this year. However, it’s safe to say that derivative risks usually involve:

Value risk – In most cases it’s almost impossible to know a derivatives “true” value. The risk here is uncertainty about how others will value that derivative now or in the future.

Easy Leverage – One or more parties involved in a derivative often use borrowed money (or leverage), which is relatively easy to obtain. Putting up only one dollar for every 8 or 10 dollars in the contract is not unusual. Easy access to leverage compounds the potential size of derivative losses.

Time Restrictions – Most derivatives have a time component. So, you can have the right investing thesis (e.g., oil prices will go up by 10%) but still lose money because your timing was wrong (e.g., oil prices went up a month after your contract expired). Unlike long-term stock or bond investing, derivatives force you to engage more actively in market timing, which is essentially impossible with any consistency.

It’s certainly possible to make money through derivatives; it happens everyday. But the complexities involved combined with the substantial risks of losing money brings me back to the same conclusion I had in my last post about obscure alternative investments. Specifically, a rational and objective assessment suggests that acquiring the necessary expertise in one type of derivative or another involves a similar level of effort as starting a new business. And this blog is primarily about investing your savings from your existing profession without having to moonlight on a second line of work.

Collectibles and Art

Judging from all the television shows about collectibles like Antiques Roadshow, American Pickers, Pawn Stars, and Storage Wars (to name but a few), people love the idea of making money on collectibles and art. There are an amazing array of things you can buy that have the potential to appreciate in value over time. Here’s a less than exhaustive list based on some quick internet research:

Fine art paintings, lithographs, prints, photographs, sculpture etc.

Pop, folk, tribal, and ancient art

Jewelry and watches

Stamps

Coins

Antique furniture, home furnishings, and decor

Rare automobiles, motorcycles, and other transportation

Rare arms and military memorabilia

Comic books

Baseball cards

Rare toys and games

Pop and sports memorabilia

Rare books, manuscripts, maps, and historical documents

Rare musical instruments

Wine

While the television shows create hopes of finding that million dollar treasure collecting dust in the garage or attic, in the real world (as opposed to reality television) that almost never happens. On the other hand, if you already have specialized knowledge through a hobby or interest such as collecting baseball cards or comic books, it’s certainly reasonable to buy collectibles as an investment.

Returns – Because of the diversity of things you can collect, it’s impossible to say what the “typical” returns on collectibles are. And unlike the stock market, where you can get a price quote in any given minute, collectibles are exchanged in much more esoteric and location-specific ways. So, determining a fair value for collectibles is often extremely difficult. The value is often entirely in the eye of the potential buyer. The only safe generalization is that, the more knowledge you have about an item, or can buy from an expert, the greater the potential returns. And the less knowledge you have, the less likely you’ll make a decent return. Further, costs eat into returns, and the costs associated with investing in collectibles and art are generally higher than for mainstream investments. Collectible investing costs can include research time, broker fees, expert help, appraisals, insurance, marketing, maintenance, restoration, and storage.

Risks – Given the esoteric nature of collectible and art markets, the values of most of these items are much more volatile than stocks. Because of changing trends in tastes, styles, and interests, things that were once highly prized can become quickly worthless and vice versa. Additional risks for collectibles and art include:

Illiquid – Collectibles and art may have an expected value only at certain times, places, or when you can find a particular kind of buyer. It may take a long time before the perceived value is realized with a sale.

Counterfeits/Fraud – Imitations and misrepresentations exist for almost all types of collectibles and art, and some are very hard to detect.

Condition/Loss – Value is highly dependent on condition, and flaws or wear that seems unremarkable to you can greatly impact value. And of course the value of all your collectibles could be wiped out in one basement flood, unless you buy insurance, which eats into your returns.

For most of us, collecting fine art or expensive antiques is financially impossible. So, it’s also worth noting that collectible and art funds have sprung up in recent years. These private funds are purportedly run by experts that buy and sell the physical collectibles or art. By investing in one of these private funds, you are essentially owning a small piece of many pieces of art. As compared to owning stock funds, art and collectible funds costs are often excessive, such as 1% to 3% in annual management fees plus a 20% cut of all profits.

Taxes

Before investing in any of these three alternative investments, be aware that the tax rates on profits are different than stock long-term capital gains and qualified dividends, which are most commonly taxed at a rate of 15%.

Peer-to-Peer Lending – The IRS taxes interest payments as ordinary income. So, most people will pay more tax on this income than they would on long-term stock capital gains and qualified dividends.

Collectibles and Art – The IRS taxes profits from sales of collectibles or art held more than one year at a relatively high rate of 28%.

Conclusions

In my last post on alternative investments, I summarized the conclusions for each type of investment on a mindfulness scale from 1 (least mindful) to 10 (most mindful). Here’s the same summary for the three alternative investments discussed above:

Peer-to-Peer Lending – Has a current return that is similar to or less than the expected return for stocks. The risks are like diversifying a portfolio with high-yield bonds, but peer-to-peer lending has some added risks due to the newness of this business model. Mindfulness score = 3

Derivatives – Have the potential for huge rewards and huge losses. Your potential success with derivatives is largely dependent on your willingness to spend large amounts of time and energy becoming an expert in one of these derivatives. It also requires a fair amount of luck because derivatives require market timing decisions. Mindfulness score = 1

Collectibles and Art – Have unpredictable potential returns and losses that are also highly dependent on your knowledge in one of these areas. If you already have an interest in one of these areas, or think you might enjoy learning more, collectibles or art may be a reasonable form of portfolio diversification. But it certainly seems unwise to concentrate too much investing capital in one of these esoteric markets. Mindfulness score = 2.

Like my conclusions for annuities, commodities, currencies in my last post, it’s pretty clear that your investing diet shouldn’t contain too much peer-to-peer lending, derivatives, or collectibles and art. To the extent you think it could be fun to devote the time needed to successfully invest in peer-to-peer lending or collectibles and art, it might make sense to devote 5% or 10% of your investing capital in one of these areas. In contrast, derivatives seem like empty calories that are mainly just risky to your investing health.

* The original meanings and later translations of this word are interesting, as discussed here.