ATM INVESTMENTS Disclaimer: This is not a solicitation to sell securities, which is only done through appropriate disclosure documents and only to qualified investors. We are not financial advisors, nor attorneys, nor accountants, nor do we hold ourselves out to be so. Nothing on this website should be interpreted as a recommendation. investors are encouraged to consult with their personal legal and tax advisors. Neither this website nor its representatives, officers, employees, affiliates, sub-contractors or vendors provide tax, legal or investment advice. Nothing on this website is intended to be or should be construed as such.

We sat down for coffee and soon began to talk about investing.

“Well, the most recent investment I made was another tranche of $52k into an ATM fund”, I told my friend.

His response was typical. One raised eyebrow, a quick blink as he did a double take, and then a couple seconds later, his reply: “What? Why… what do you mean?”

No surprise. It isn’t obvious how ATMs – yes, automated teller machines, those! – could even be called an investment. What would you be investing in, and does this mean the investor is shuttling cash around the city in armored cars, withdrawing from here and depositing there?

As we’ll get to: buying, placing, funding, and operating your own ATM is a valid strategy. This article isn’t primarily about how to start an ATM business, but we’ll direct you toward resources that can help, if you want to go this route.

Instead, this article is mostly about how I passively invest in ATM funds, and earn a 14-16% Internal Rate of Return on my capital (and an even higher Cash On Cash return), in a very tax-deferred way. Completely legally.

Of course, the main friction point is the set of risks this comes with. First, you need to be an Accredited Investor to invest passively in ATM funds. If you’re not accredited, then you should first try to become so. But why do you need to be accredited? Because the risks of ATM investing are much less obvious than the risks of buying ETFs and public stocks, and the government doesn’t want people who can’t afford to lose money, to be sucked into

For me, this means I don’t want to allocate more than 5-10% of my portfolio to ATM funds. For you, this might mean something different.

Let’s get into it.

Rather watch a Youtube video about this? Click below.

What does it mean to invest in ATMs?

Like any investment, you must understand what it is exactly that you’re getting into.

The primary revenue stream of an automated teller machine, or “ATM”, is the transaction fee. You know… the $2-3 you have to pay to withdraw cash from an ATM. Stack 10-20 transactions a day, and you have a perfectly viable and understandable small business.

A single well-placed ATM in a high-traffic area should yield between $800 to $1,300 per month in revenue.

What’s a high-traffic area? It should be obvious if you start paying attention to this in your daily life: Pharmacies, cannabis dispensaries, music festivals, casinos, bars, grocery stores, etc all often have ATMs on-site, where you can withdraw cash if you need to. Banks have them too of course, and as we’ll see later, some ATM investment fund operating companies also serve banks.

Don’t take that as gospel, of course. If you buy your own ATM (we’ll get to that in a minute), you might easily lose money on it, if you aren’t good at placing machines or establishing agreements with property owners who will rent you space to put them in.

Think of it this way: operating an ATM is essentially a retail micro-business, with an average transaction size of a few bucks, and no full-time employees to manage. If you can do it with one machine, you can do it with 10, 100, or thousands. There are about 450,000 ATMs in the United States at the moment, and a few million around the world.

Like any business, it can have investors.

The question for you is: do you want to be the one hustling around the city with cash, and earning much more of your fee revenue? Or do you want to invest passively in a fund that does this for you and takes a cut?

Active Investing as Owner/Operator: Should You Buy ATM Machines?

You can find videos aplenty on Tiktok purportedly showing you how to start an ATM business as a side-hustle. And what a hustle it is… every few to several days, you’re getting more cash from the bank to deposit to your ATM, so it doesn’t run out of money. It’s not that this is an invalid way to make money, but at this point, you’ve bought yourself a job. And a very effortful one, at that.

How much do ATM owners make? About $450-700 per ATM per month, if they’re independent and can place their machines in at least moderately good locations. And you’re in control of your “jobvestment”, which is a nice bonus. Unless you physically get robbed (possible, of course), you know that nobody’s stealing from you.

But there are a few problems with this jobvestment that you’ve bought yourself:

- If you want to hire, you better REALLY trust your employees. They’re shuffling your cash around the city for you. Better dial in your audit procedures.

- If you don’t hire this out, good luck taking a vacation. Ever.

- You need a lot of ATMs to make this profitable.

- You’re going to need to be really good at sales to build up the relationships you’ll need with property owners, to convince them to lease their space to little ol’ You, and not your Much Bigger ATM Operator Competitor. You might need to outbid the bigger competitor, or just settle for lower-quality spaces. As a fun exercise: pretend you already own an ATM, and cold-call the 20 most likely possible locations in town. I bet you 19/20 of them already have an ATM, or won’t deal with you even if they might have space available.

- Your bookkeeping is going to suck. Cash based businesses are prone to IRS audits, too. Not to mention Independent ATM Deployer (IAD) audits, if you’re certified.

And then some.

As an experienced entrepreneur myself, I can tell you this: there are much easier businesses to run in this digital age, that don’t require rucking bags of cash around the city.

So, despite the risks of passive ATM investing (primarily: giving up control), I do invest in ATMs through funds. I just don’t put more than 10% – maybe temporarily 15% – of my portfolio in them at any given time.

Passive Investing In ATM Funds: Risks To Know Before You Invest

In the passive investing model, you’re not buying your own ATMs, you’re not stocking them with cash… you typically don’t even know exactly where the ATMs that the fund operates, are. You’re an investor in a fund whose business is to owns and operates ATMs, take a cut, and pay out some of that to you. Suddenly, the picture changes: you’re staking your investment on the belief that the fund operator is better than you would be at the whole game of buying, placing, updating, managing, funding, and supporting ATMs. You’re hoping that, with their institutional knowledge and their master service agreements with Walgreens chains and grocery store conglomerates, they’ll have operational efficiencies that you couldn’t have as an independent operator with your own “paper route” and your 5-20 machines you bought on a marketplace site.

But you’re also hoping that the fund doesn’t become a Ponzi scheme, and that its operators remain honest. In fact, it’s a pretty safe bet that anyone experienced in the ATM business would be “better at it” than I would, with no ATM management experience. The biggest risk in passive ATM investing is actually the fund managers’ integrity. This is a far bigger risk than the macro risk of a widespread and immediate reduction in the use of cash (and therefore ATMs) in the United States – which is still a risk, but in my view a smaller and more manageable one than the Ponzi scheme risk.

Ready to take that risk – which is a factor in all investments but an even greater priority in private ATM investing? For me and for other investors I know, the potential rewards of this asset class make the risk worth taking. Read on for more details about the returns and tax benefits being offered by ATM funds.

Speaking of knowing the operators you’re dealing with: one of the interesting tidbits you’ll learn about this space is that almost every website you will come across offering ATM fund investing, is actually a feeder for a company called “The Real Asset Investor”.

Who is The Real Asset Investor?

Founded by Dave Zook in 2015, The Real Asset Investor is a niche investment fund. Their strategy is to find asset classes that produce cash flow and/or equity growth, with preferential tax treatment. And ATMs have been one of their most popular investment offerings since then. Essentially, TRAS brings in capital, and deploys it with the ATM operator, Paramount Management Group, which is a pretty run-of-the-mill-looking managed services business, per their LinkedIn, focused on automated teller machines. There are shareholders from TRAS on the board of PMG, and vice versa.

If you’re passively investing in ATMs, there’s a good chance that Dave Zook’s company or its affiliates are raising money to be deployed in Paramount’s ATM management model. I say all this merely to let you know who the players are and what’s happening with your money when you invest it.

Like I touched on above: the biggest risk isn’t that Paramount is bad at operating ATMs, the risk is that TRAS or PMG end up becoming fraudulent. As best we can tell, based on the fact that Paramount acquired another ATM company back in February 2023, and because Paramount’s activities are audited by a bank, they seem to be a normal, healthy operating business.

As always, with any private syndication but especially with one that is somewhat opaque and cash-based where there isn’t one single property you can just go visit in person (like a multifamily syndication), keep your eyes peeled and don’t assume that an honest fund operator won’t later become dishonest, down the road. It’s happened before, and it will happen again. And do your own diligence on any ATM investments you make.

Now, let’s get to the good part: what are the potential advantages of investing in an ATM fund?

Advantages of Investing in ATM Funds

Investing in ATMs, even indirectly via a fund, can offer investors several advantages, especially if they are interested in generating a predictable cash flow. Here are some of the reasons why:

- The asset value doesn’t matter. Who cares if the ATMs go down in value? In fact, we expect them to. We expect the ATMs to be pretty much obsolete and valueless, within several years. We’re not investing in ATMs for their asset prices, we’re investing in the cash flow stream that comes from the transaction fees. Relatedly…

- Accelerated tax depreciation. ATMs depreciate in value very quickly, and as of the time of this writing, at least for my own situation, 60-80% of the value of my investment can be expensed as depreciation in the first year. The rest is depreciated in the the handful of years following the first. Got any passive

real estate income? This depreciation expense can be a significant write-off against that income, kicking the tax can down the road. Consult your tax professional with any questions on this: I’m not a CPA, I’m just my CPA’s client. - Predictable Income. ATM investments, at least through The Real Asset Investor, pay me a fixed monthly return starting in 2-4 months after the investment is made. They deposit these payments via ACH directly to my bank. This is very similar to the structure that PPR offers, and that you can get with buying high-quality real estate notes.

- No Asset Management Labor. There’s literally no work involved apart from making sure that the payments arrive on time.

- Higher-Than-Average Yield. Without even factoring in tax depreciation, ATM fund investments offer advertised cash-on-cash returns of over 24% per year, despite there being little to no return of principal at the end of the 84-month term. Even factoring in the lack of returned principal, the advertised IRR can come in north of 14% per year. That’s lower than many

real estate syndication operators offer, but the cash flow compounding aspect is the real magic factor in play. Principal is expected to be paid back within a few years, and the rest is gravy. - Diversification. Investing in ATM funds can offer a way to diversify an investment portfolio, and improve cash flow. They offer a different risk-reward balance than stocks, bonds, or traditional

real estate investments, which might reduce overall portfolio risk. - Low Correlation with Markets: ATMs are not correlated with stock and bond markets, which makes them a good diversifier in a portfolio. In periods of stock market volatility, these notes can provide a more stable source of income. The main risk here is that people stop using cash in extremely significant quantities; but, while you and I probably rarely use cash, significant segments of the population still use cash quite a bit.

- Passive “Mailbox Money” Income: The best advantage of all! Once the ATM investment is made, there’s no work required of you as an investor.

These advantages, for me, outweigh the very crucial risks, as we delved into above.

ATM Investments: Advertised Returns

As the fund’s website clearly states:

IMPORTANT: The projections or other information generated by the cash flow model above regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results.

Pay close heed to that disclaimer. Nothing in business or investment is guaranteed. With that being said… the following table of returns is advertised by the most popular ATM investment fund available today.

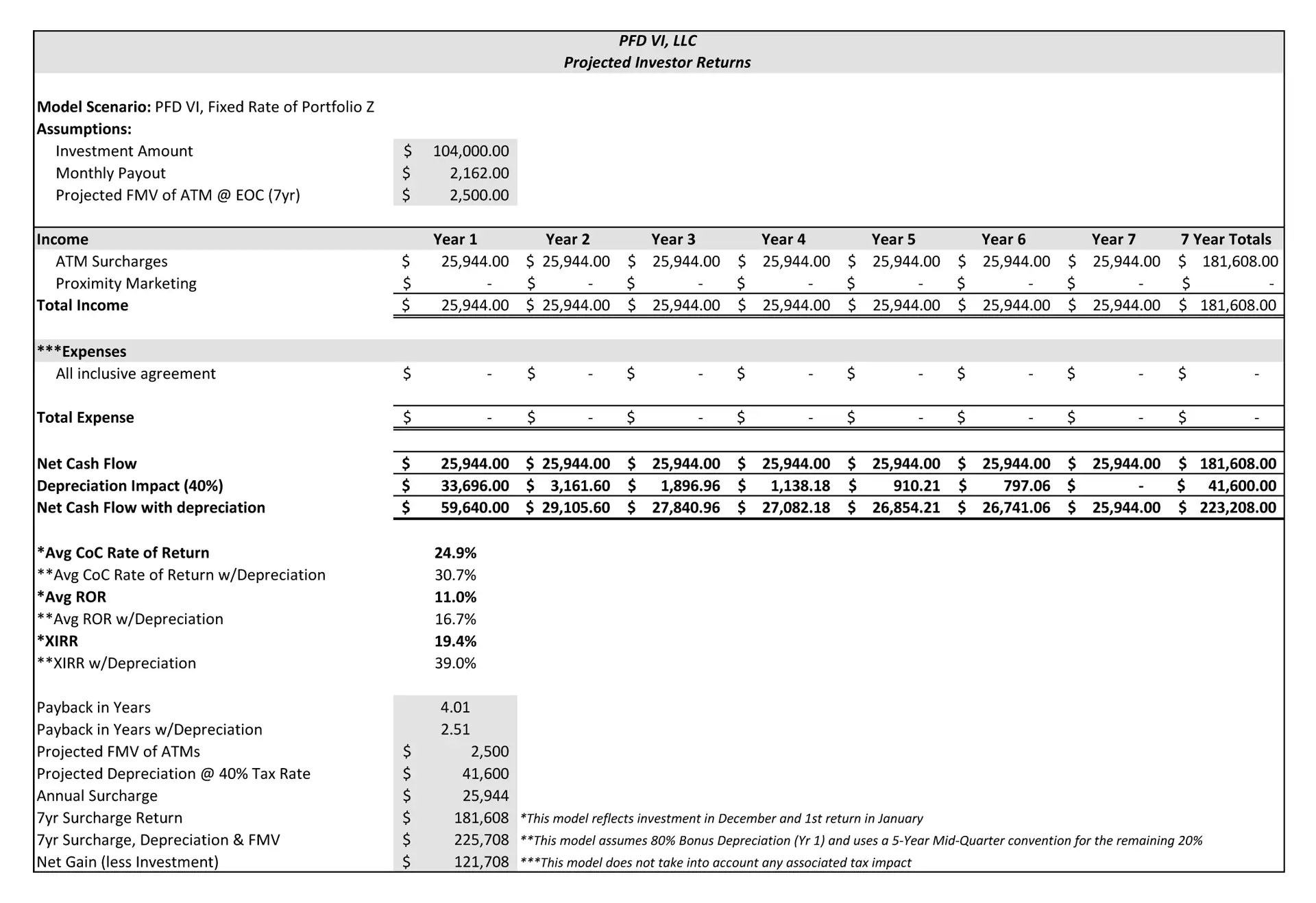

Our Pick

ATM Fund Investment Model

ATM Fund Investment Model

A full model to help you calculate the projected, advertised returns of the ATM fund I've invested in. Past performance does not guarantee future results.

Download Now

A full model to help you calculate the projected, advertised returns of the ATM fund I've invested in. Past performance does not guarantee future results.

Conclusion

My view as an investor in this fund is that ATM investments are worthy of a small percentage of my overall portfolio, for a few reasons: the amount I’ve invested cumulatively is one I can afford to lose; the bonus depreciation will defer my taxes payable on this and other passively-earned income; the cash flow begins quickly and lets me compound my gains by reinvesting it earlier, elsewhere; and of course, the overall rate of return is quite good. It solidly fits my goal of earning passive, tax-advantaged income without adding more work to my plate.

Good luck, do your own diligence, and remember: I’m an investor, not a financial advisor. Go make your own mistakes, and also, if you can: make a bunch of your own money.

This is easily the most thorough breakdown of this investment class that I’ve ever seen. ATM funds have been one of my top, most consistent performers!