Most people should have a forward-looking investment plan that describes their investing goals and how they intend to reach those goals. For example, if your investment plan focuses on retirement, you’ll need to answer questions like:

- How long will it take until your ready to retire?

- How much will you be able to spend each year during retirement?

- How long will your money last after you retire?

To answer these sorts of questions, you need to estimate the potential future growth of various investment options. In investment lingo, you need to predict your long-term “return”. For this reason, I track published estimates of the expected future returns for stocks, bonds, and cash.

Predicting the Future

One method to estimate future returns is to look back at historical returns and assume those returns will continue into the future. To support this method, I recently posted an update on historical returns for stocks and bonds including tools to estimate returns for any past period going all the way back to 1871 for stocks and 1926 for bonds.

Another method to estimate future returns is to predict, or forecast, based on current economic and market conditions. In this post, I present updated stock and bond return forecasts recently published by eleven different investment advisers. To make their forecasts, these companies use various models and algorithms that I won’t attempt to explain here. Of course, it’s impossible to predict the future exactly, even using complex-sounding models. So, be careful about how you use these return forecasts in your investment planning.

Summary of Return Forecasts

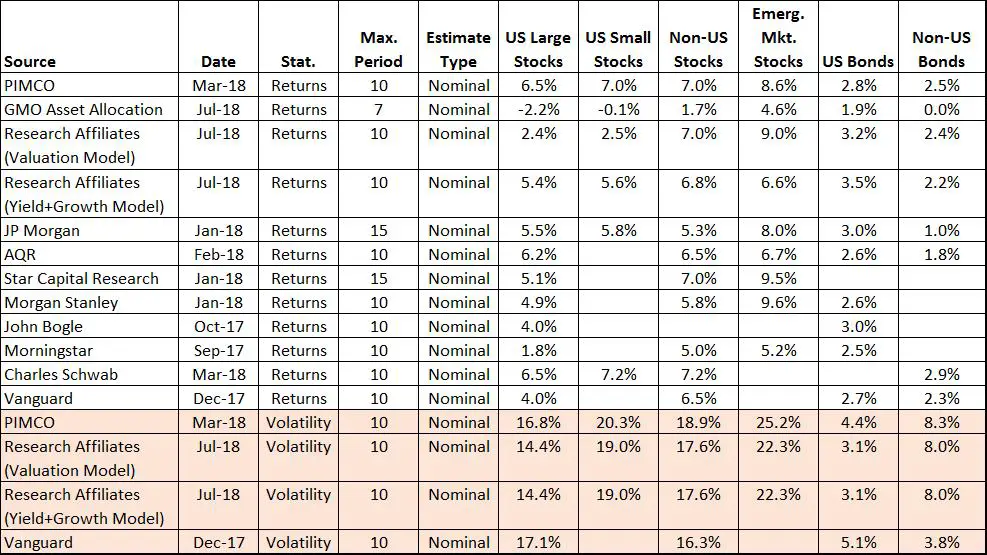

I reviewed multiple websites and news articles for possible sources of return forecasts from reputable investment companies. I’m sure my resulting database is not exhaustive, but I didn’t find any more comprehensive summary on the internet. This table summarizes the forecasts of nominal (not inflation adjusted) annual returns over a specified future period ranging from 7 to 15 years.

In a few cases, I extrapolated nominal returns from real return estimates using the inflation assumptions specific to the forecast. The tan-colored bottom rows of the table show volatility (standard deviation) estimates that were also available from four of theses sources, which I’ll discuss in the next section.

I often read on personal finance blogs and online forums that the stock investor should expect an 8% to 10% annual return on average, because that’s the historical long-term return for the U.S. stock market. The Reddit boards seem particularly prone to these historically-based assertions. However, the table above shows that most professional investors are assuming U.S. stock returns in the next 7 to 15 years that are more in the 7% to -2% range.

Here’s a graph that shows the ranges of the return forecasts by asset type.

These companies are consistently forecasting that international stocks (both developed and emerging markets) will outperform U.S. large cap stocks. Conversely, U.S. government bonds are generally expected to outperform international government bonds, if only slightly. The other notable pattern is that the range of bond estimates is much narrower than the range of stock estimates. This is probably because changes in bond returns are more predictably correlated with larger economic changes in inflation and interest rates. And for good or bad, these companies seem to be using similar economic assumptions.

GMO’s forecasts are particularly sobering given they had the lowest return estimate for every asset type, and they were the only company predicting a loss (negative return) for U.S. large cap stocks. GMO seems famous for this, because I found several references to GMO’s “perennially bearish” predictions.

Forecasts of Return and Volatility

As I mentioned, four of these companies also provided forecasts of volatility in terms of standard deviation. We can see the combined return and volatility estimates using the classic cross-plot of “risk” versus “reward”.

As would be expected, bonds have a much lower expected volatility as compared to stocks, but also a much lower expected return. The range of the projected stock volatilities is relatively narrow, while the stock return estimates vary by a wider margin, except international stocks. It’s somewhat surprising that the U.S. stock volatility estimates are so uniform, given that estimates of lower stock returns implies that market crashes, which typically boost volatility, are expected in the future. My best guess is that these models probably assume that more volatile crashes will occur within brief periods of the overall 7- to 15-year forecast window.

While most of these forecasts are estimates from particular models, PIMCO’s return and volatility estimates are based on a survey of “defined contribution consultants”, who presumably used whatever methods they each preferred. Because PIMCO’s crowd-sourcing approach aggregates many forecasting methods and assumptions, it’s worth a closer look. The report includes this nifty graphic that shows the median responses of 39 consultants in the survey.

Although the report doesn’t describe the ranges or distributions of the responses, the median responses tend to lean toward the high end of the ranges from the other forecasts. “Defined contribution consultants” seem to be a somewhat optimistic bunch, but they’re still predicting lower returns than the historical averages. The PIMCO graph also provides return and volatility estimates for commodities, REITs, and TIPS, which weren’t often addressed by the other forecasts.

Forecast Uncertainties

As I’ve written before, these forecasts are notoriously uncertain. Scientists like me find it useful to distinguish between uncertainties of precision and uncertainties of accuracy. You can think of precision as a measure of how tightly the archer’s arrows were grouped on the target, while accuracy is a measure of how close the arrows came to the bull’s-eye. Lets look at each uncertainty.

Precision – One way to measure precision is through the differences between the forecasts, which are most likely caused by the different models and methods used. For example, the U.S. large cap return forecasts across the studies range from about -2% to 7%. So, selecting any single “best” forecast (using whatever criteria you want to dream up) could lead you to conclude that your retirement plan is anywhere between a rousing success and a dismal failure. In other words, the forecasts are not particularly precise.

A second way to measure precision is within each forecast, because different reasonable variables or assumptions can be applied to the same model. Most of these forecasts present surprisingly little precision information. I guess the forecasters assume that investors are seeking an unequivocal “best estimate” from an expert. Vanguard was one of the few studies to offer any meaningful precision information, which I eyeballed from a chart and summarized in this table.

| Vanguard Return Forecast | 25th Percentile | 75th Percentile | Range |

| US Large Stocks | 2% | 7% | 5% |

| Non-US Stocks | 4% | 8% | 4% |

| US Bonds | 2.5% | 3.5% | 1% |

| Non-US Bonds | 1.8% | 3.3% | 2% |

I used the 25th and 75th percentiles to represent the most likely outcomes. (The study also presented 5th and 95th percentile estimates, which were much wider.) The study’s internal precision for bond forecasts is pretty good. But the stock forecasts range widely enough to be almost useless, particularly if you consider that the range from 25 to 75 percentile covers only half of the possible outcomes from the Vanguard model.

Star Capital also looked at how precise their estimates were by propagating the uncertainties in terms of future S&P 500 stock values, as shown in this graph.

So, the most likely range of the Star Capital outcomes has the S&P 500 growing from 2,500 in December 2017 to somewhere between 2,600 to 7,400 by the year 2032. However, Star Capital says the tighter band of 3,400 to 5,300 “seems probable”. Regardless, if you applied either of these ranges to your retirement plan, your conclusions could again range between very encouraging to very discouraging.

Accuracy – We can judge the accuracy of these forecasts by comparing past forecasts to what actually happened. If the forecast turned out to be the same as actual returns in the next 7 to 15 years, then that would be a bull’s-eye for forecast. None of these studies compared their past forecasts to actual outcomes, because I’m sure they were afraid it would make them look like idiots. However, I found two other posts that made accuracy comparisons.

Charlie Biello compared the previous GMO 7-year forecast to actual subsequent returns as summarized in this table.

| Previous GMO Return Forecast | Forecast | Actual | Difference |

| US Large Stocks | 2.7% | 13.2% | 10.5% |

| US Small Stocks | 0.1% | 12.0% | 11.9% |

| Non-US Stocks | 6.1% | 4.7% | -1.4% |

| Emerging Market Stocks | 7.6% | 0.7% | -6.9% |

| US Bonds | 2.8% | 2.5% | -0.3% |

| Non-US Bonds | 1.2% | 0.1% | -1.1% |

Again, the bond estimates were reasonably accurate, while most of the stock forecasts missed the target entirely.

Similarly, Larry Swedroe compared past forecasts by his firm, Buckingham Strategic Wealth, to actual outcomes. (I didn’t include Buckingham’s forecast in the above summaries because I couldn’t find a full report anywhere on the internet.) Here’s a table comparing forecasts of global

| Swedroe Global Market Stock Return Forecast | Forecast | Actual | Difference |

| 2003 to 2018 | 7.2% | 11.2% | 4.0% |

| 2004 to 2018 | 7.2% | 9.5% | 2.3% |

| 2005 to 2018 | 7.2% | 9.1% | 1.9% |

| 2006 to 2018 | 7.0% | 9.0% | 2.0% |

| 2007 to 2018 | 7.1% | 8.0% | 0.9% |

| 2008 to 2018 | 7.1% | 7.8% | 0.7% |

These forecasts appear considerably more accurate than GMO’s last forecast. But with a backward looking comparison, we don’t know whether a Buckingham forecast of today is likely to be off by 4% or only 0.7%. And if we consider wider uncertainties associated with predicting the future, there’s certainly no guarantee that their next forecast will be more accurate than their earlier forecasts.

Conclusion

You’re probably thinking that these forecasts are so imprecise and inaccurate that using them at all would be a mistake. In a broad sense, I agree with you. On the other hand, the experts seem to agree that the next 10 to 15 years of returns will be substantially below historical norms. Although all these forecasters could be wrong, it seems particularly imprudent to use historical average returns in an investment plan now. After all, if you happen to under-estimate your actual returns, you probably won’t regret that decision. But blithely assuming you’ll get the 8% to 10% returns of the past could result in the biggest regret of your lifetime.

So, how far below the average historical returns should we estimate? There’s obviously a lot of judgement involved here, and some of that judgement is going to change with the specifics of your situation, like whether you have 30 years or 5 years until you hope to retire. I can’t tell you exactly what value to use within all these forecast ranges.

However, I can at least use my situation as an example. I fully retired at the start of this year with a decent nest egg. My main investment goal is for the money to last the rest of my and my wife’s lifetimes, however long that is. If I assume a high future return, we can spend like crazy. If I assume a really low return, we need to tighten our belts for the next few years until we see how things develop. Our portfolio is 80% diversified stocks and 20% cash (high yield savings account), for reasons I detail in my “investing over time” series of articles. The stocks are 60% U.S. and 40% developed and emerging markets, for reasons I detail in my stock diversification article.

Given all this, I’m using 5% as base case future return for my stock portfolio. (I also run an uncertainty analysis using different average annual returns and sequences of returns, but that’s a post for another day.) An estimate of 5% seems reasonably conservative to me without being extremely pessimistic. Specifically, if I exclude the GMO forecasts*, the U.S. stock forecasts are in the range of 2% to 7% range, developed markets are in the 5% to 7% range, and emerging markets are in the 5% to 9% range. If my portfolio was entirely in U.S. stocks, I’d probably drop my base case estimate down to 4%.

Of course, the future return you select is entirely up to you. My advice is that a more cautious (but not overly pessimistic) estimate will allow you to plan prudently and is less likely to cause unpleasant surprises in the future.

* I’m ignoring the GMO forecasts because they’re a consistently low outlier, and they also had terrible accuracy in the last 7 years.